Management needs to investigate and solve the issue by reducing the actual time spend or revising the standard cost. Before production, the company needs to prepare the product standard cost. The standard cost usually includes variable costs such as direct material and direct labor. In order to make a proper estimate, management estimates the standard cost base on the unit of labor and material. For example, one unit of cloth requires 0.1Kg of raw material and 1 hour of labor. After getting multiple quotes, you have determined that the standard cost of the job will be 20 hours of labor at $60 per hour.

Direct Labor Yield Variance FAQs

That’s best done after considering the most common sources of inefficiency. Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting. Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping.

Related AccountingTools Course

A financial professional will offer guidance based on the information provided and offer a no-obligation call to better understand your situation. Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs. Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications.

Why is it important to calculate direct labor yield variance?

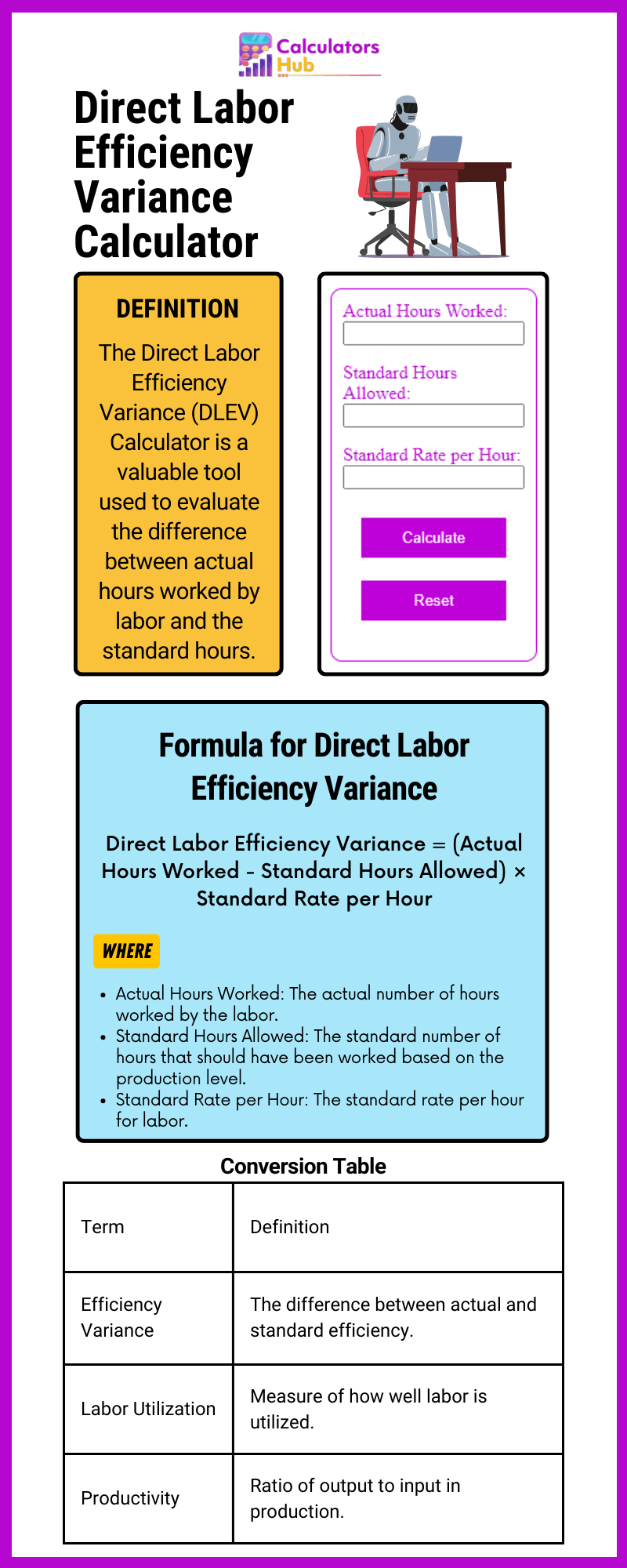

With either of these formulas, the actual hours worked refers to the actual number of hours used at the actual production output. The standard hours are the expected number of hours used at the actual production output. If there is no difference between the actual hours worked and the standard hours, the outcome will be zero, and no variance exists. With either of these formulas, the actual rate per hour refers to the actual rate of pay for workers to create one unit of product. The standard rate per hour is the expected rate of pay for workers to create one unit of product. The actual hours worked are the actual number of hours worked to create one unit of product.

When the job is finished, you find that you paid for 33 hours of labor at $60 per hour. When you plug this into the formula, you get a direct labor efficiency variance. Direct Labor Efficiency Variance is the measure of difference between the standard cost of actual number of direct labor hours utilized during a period and the standard hours of direct labor for the level of output achieved.

In this case, the actual rate per hour is \(\$9.50\), the standard rate per hour is \(\$8.00\), and the actual hours worked per box are \(0.10\) hours. This is an unfavorable outcome because the actual rate per hour was more than the standard rate per hour. As a result of this unfavorable outcome information, the company may consider using cheaper labor, changing the production process to be more efficient, or increasing prices to cover labor costs. The direct labor rate variance is the $0.30 unfavorable variance in the hourly rate ($10.30 actual rate Vs. $10.00 standard rate) times the 18,400 actual hours for an unfavorable direct labor rate variance of $5,520. In other words, when actual number of hours worked differ from the standard number of hours allowed to manufacture a certain number of units, labor efficiency variance occurs.

- Secondly, hiring and training need to take labor efficiency into account.

- What we have done is to isolate the cost savings from our employees working swiftly from the effects of paying them more or less than expected.

- Organizations can use DLYV to identify cost-saving opportunities, measure the productivity of their labor force, and improve operational efficiency.

The standard direct labor hours allowed (SH) in the above formula is the product of standard direct labor hours per unit and number of finished units actually produced. In Company Zeta’s case, actual labor hours significantly exceeding the standard hours indicate inefficiencies in labor use, leading to additional labor costs. Conversely, fewer actual hours than standard would denote improved efficiency and cost savings. Labor efficiency variance, also referred to as labor time variance, constitutes a segment of the broader labor cost variance. This variance emerges from the disparity between the anticipated standard labor hours and the actual hours expended. Its core function lies in quantifying this difference, providing insight into whether a business optimally leverages its labor force.

We may think that only unfavorable variance is required to solve as it impacts the profit at the end of the year. It is correct that we need to solve the unfavorable variance, however, which turbotax version should i use in 2021 the favorable variance also required to investigate too. Favorable variance means that the actual time is less than the budget, so we need to reassess our budgeting method.

If there is no difference between the standard rate and the actual rate, the outcome will be zero, and no variance exists. Direct labor efficiency variance is a financial metric that takes the standard labor hours estimated during the planning phase of a project and compares them with the actual direct labor hours that have been used. It is very important to measure how close you are to what you expected in order to determine how well labor is utilized on a jobsite. This variance shows how efficient labor is, comparing it to the standards set in the first parts of the planning phase. Controlling these costs is essential, and one of the key ways to do this is through calculating direct labor efficiency variance.

If the outcome is favorable, the actual costs related to labor are less than the expected (standard) costs. Watch this video presenting an instructor walking through the steps involved in calculating direct labor variances to learn more. In manufacturing, efficiency variance can be used to analyze the effectiveness of an operation with respect to labor, materials, machine time, and other production factors.

By the end, you’ll be able to understand how this measurement can improve your project’s labor costs, which means that it will ensure a more profitable outcome. If customer orders for a product are not enough to keep the workers busy, the production managers will have to either build up excessive inventories or accept an unfavorable labor efficiency variance. The first option is not in line with just in time (JIT) principle which focuses on minimizing all types of inventories.